Quick Links

Tax increment financing (TIF) is the key tool of an urban renewal authority to support and attract new development and investment. This tool can only be accessed through established urban renewal areas (plan areas). This section will describe what TIF is, how TIF works and the process for establishing new plan areas or projects to use TIF. Within the bounds of the statutory and financial requirements, CSURA has discretion to determine the projects it approves.

Tax Increment Financing

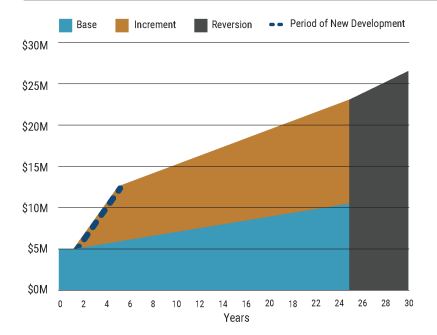

TIF is the increment or difference between the original tax revenue (also referred to as the base value) and the new tax revenue within the plan area that increased due to new development and investment. TIF is a significant funding resource to affect change. The use of TIF requires approval of each taxing entity within the plan area and can apply to property tax and sales tax for up to a 25-year period. The approval of TIF directs the new increment of tax into an urban renewal area or plan area, which can then be deployed by CSURA to close the financial feasibility gap of a proposed project, mitigate blight, and fund public improvements. All projects must fulfill State Statute requirements to prove eligibility. This is further described in the next section.

TIF is the increment or difference between the original tax revenue (also referred to as the base value) and the new tax revenue within the plan area that increased due to new development and investment. TIF is a significant funding resource to affect change. The use of TIF requires approval of each taxing entity within the plan area and can apply to property tax and sales tax for up to a 25-year period. The approval of TIF directs the new increment of tax into an urban renewal area or plan area, which can then be deployed by CSURA to close the financial feasibility gap of a proposed project, mitigate blight, and fund public improvements. All projects must fulfill State Statute requirements to prove eligibility. This is further described in the next section.

How TIF Works

Existing Tax Base

When TIF is initiated, the tax base is frozen or set at the current year’s level. This base amount will only increase a minimal amount biannually for property tax to account for inflationary adjustments in value. This base amount will continue to be collected by each tax district over the TIF timeframe (maximum of 25 years).

New Development

A developer fulfills the URA Plan’s vision by developing property within the plan area. This new development generates additional value, which is referred to as increment.

The increment can be in associated with increased land value from horizontal infrastructure improvements, improvement value from vertical development and retail sales from new commercial development.

Increment and Revenue

The tax increment is the difference between the base tax revenue and the new tax revenue from development.

- Increment

- New Development Value

- Base Value

The corresponding assessment rates, mill levies, and sales tax rates for the property are applied to the incremental value generated to translate it into tax revenue.

These are not existing tax dollars; the increment would not exist without the investment of new development and the establishment of a plan area.

This incremental tax revenue is collected by the URA to deploy within the plan area based on direction from the URA Board to fund public improvements, provide gap financing to a developer, and remediate blight.

TIF Impact

- Each taxing entity continues to receive tax revenue from the original value as if no development occurred.

- The URA collects revenue from the tax increment generated by the new development.

- When the TIF timeframe ends (up to 25 years), the incremental value that has been created is released to each taxing entity to collect tax revenue in subsequent years.

Establishing Plan Areas

The ability for CSURA to create a new Urban Renewal Area (plan area) and use TIF are established by the Colorado State Statute. There are a series of criteria and requirements outlined in C.R.S. § 31-25-101 et seq. that must be met along with agreements with each taxing entity including final approval by City Council. There are three reports required to establish a new Urban Renewal Area and each requires URA Board approval.

- Existing Conditions Survey

The existing conditions survey is conducted first to determine if the proposed plan area meets the definition of blight as defined by the State Statute. Blight is attributable to a multitude of conditions which, in combination, tend to accelerate the phenomenon of deterioration of an area and prevent new development from occurring. There are 11 factors of blight that can be either observed or supported by data. These include various physical, environmental, and social characteristics found on the properties, buildings and structures, and infrastructure. The existing conditions survey documents each factor that is present within the proposed plan area. To successfully meet the criteria delineated by the State Statue and have a basis to create a new URA, one factor is required for single property ownership, four factors are required for multiple property owners. - Urban Renewal Plan

An Urban Renewal Plan is the governing document that gives powers to an Urban Renewal Authority within an urban renewal area. It is required to define the interest and intent of creating a plan area and use TIF as a tool to stimulate and leverage public and private investment. The Urban Renewal Plan sets the purpose of the URA and vision for development, remediation of blight, and use of TIF. It identifies conformance and implementation of a city’s comprehensive plan as well as all other applicable adopted plans. Most importantly, the Urban Renewal Plan authorizes urban renewal undertakings, activities, and financing powers. This includes the ability to acquire and dispose of property, enter into development and cooperation agreements, use property and sales TIF, and tax increment reimbursements. - Impact Report

The impact report summarizes the fiscal impacts of plan area development for El Paso County and all tax districts. It includes forecasted property and sales tax revenues as well as fiscal and service impacts associated with development in accordance with the Urban Renewal Plan. It specifically responds to the requirements outlined in C.R.S. § 31-25-107 (3.5). These three reports serve as tools for CSURA to use in negotiations with each tax district when identifying an appropriate level of TIF that is retained by the URA and if any portion should be remitted to the tax district.

Financial Feasibility

In addition to the foundational legal requirements, CSURA applies a financial feasibility test to determine the need and the amount of subsidy or TIF that is warranted for project gap financing. This is the “but for” test, in which a project can only move forward and be viable but for the inclusion of TIF. The financial evaluation accounts for all sources of revenue for the development including other financing sources such as metropolitan district and public improvement fee. TIF is a tool that enables development to move forward that otherwise would not occur. This test quantifies the financial hardship the project is experiencing and the appropriate amount of TIF funding to close the financial gap.

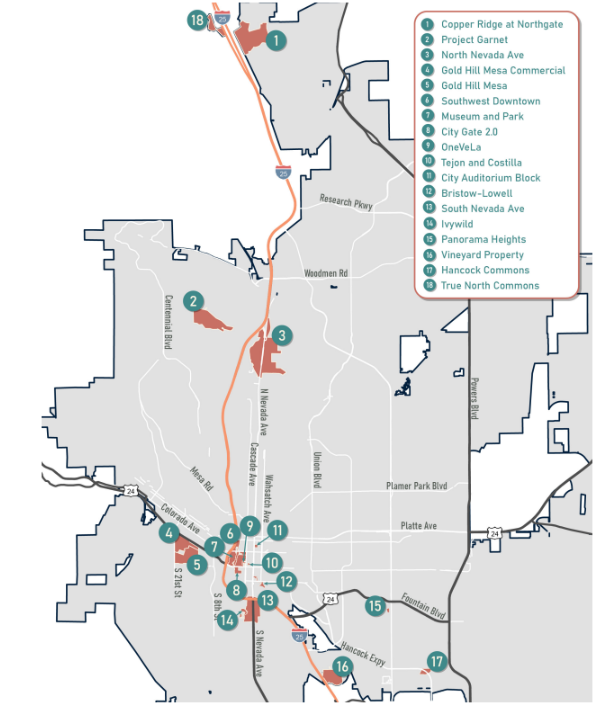

Current Plan Areas

CSURA currently has 18 plan areas adopted. These URAs are located throughout Colorado Springs with a concentration downtown (Figure 1). Each project is unique and provides community benefits. They involve a wide variety of land uses including residential of various densities, mixed use development, retail, industrial, and institutional. Many of these projects turned underutilized or damaged property into an iconic destination such as Ivywild School and Air Force Academy Visitor Center.

Figure 1. CSURA Plan Areas